A System in Transition

Kuwait’s Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) landscape is entering a more exacting phase. Legislative reform, regulatory tightening, and early enforcement signals are converging to reshape expectations—particularly for DNFBPs. For in-scope businesses, this is no longer a technical exercise. It is a question of exposure.

On 13 February 2026, the Financial Action Task Force (FATF) placed Kuwait under increased monitoring following its 2024 Mutual Evaluation. Grey listing does not mandate de-risking. But it changes behaviour. International banks are applying greater scrutiny. Correspondent banking relationships are tightening. Cross-border transactions are encountering more friction. Businesses operating in or connected to Kuwait are, in turn, facing increased commercial, operational, and reputational pressure.

What Sits Behind the Grey Listing

The 2024 assessment does not point to an absence of framework, but to limitations in how it operates in practice. Kuwait has established the core building blocks of an AML/CFT regime. The challenge lies in depth, consistency, and implementation.

Three themes are particularly relevant:

- A still-developing understanding of risk;

- National risk assessments have relied heavily on prosecution and conviction data, with more limited use of intelligence, strategic analysis, and broader information sources. This constrains the overall risk picture, particularly in relation to terrorist financing;

- Beneficial ownership frameworks in progress.

While initiatives are underway, implementation remains at an earlier stage, with continued focus required on the availability, accuracy, and accessibility of ownership information.

Uneven application across DNFBPs

Obligations are established, but awareness and practical application vary across sectors, pointing to the need for greater consistency in implementation. This combination: frameworks in place, but not yet fully embedded, is precisely what increased monitoring is designed to address.

The Direction of Travel

Kuwait’s response has been deliberate and targeted. An agreed action plan with FATF focuses on strengthening reporting in higher-risk sectors, improving beneficial ownership transparency, and increasing investigations, particularly those with a cross-border dimension. At the same time, the enforcement posture is becoming more structured.

Ministerial Resolution No. 25 of 2026 introduces a risk-based classification of violations, with materially increased penalties. Fines can reach up to KWD 500,000, and in more serious cases, suspension or revocation of a licence is now a realistic outcome, even for a first breach.

Reporting timelines have also tightened:

- 3 business days to notify the relevant Ministry of Foreign Affairs committee;

- 2 business days to report to the Kuwait Financial Intelligence Unit.

Failure to report is itself treated as a violation.

These measures are reinforced by broader policy signals. Recent restrictions on cash transactions in certain sectors, effectively limiting the use of cash and requiring payments through banking or electronic channels, underscore a clear shift towards greater transparency and control.

Taken together, this points to a system moving beyond formal compliance towards more consistent, risk-based enforcement.

Where the Pressure Is Building

For DNFBPs, the margin for error has narrowed. Deficiencies previously viewed as technical or isolated may now contribute to a broader risk profile, with direct implications for licensing.

The areas of greatest exposure align closely with FATF’s findings:

- Beneficial ownership identification;

- Suspicious transaction reporting;

- Sanctions screening;

- Internal controls.

These are no longer peripheral considerations. They are becoming enforcement priorities.

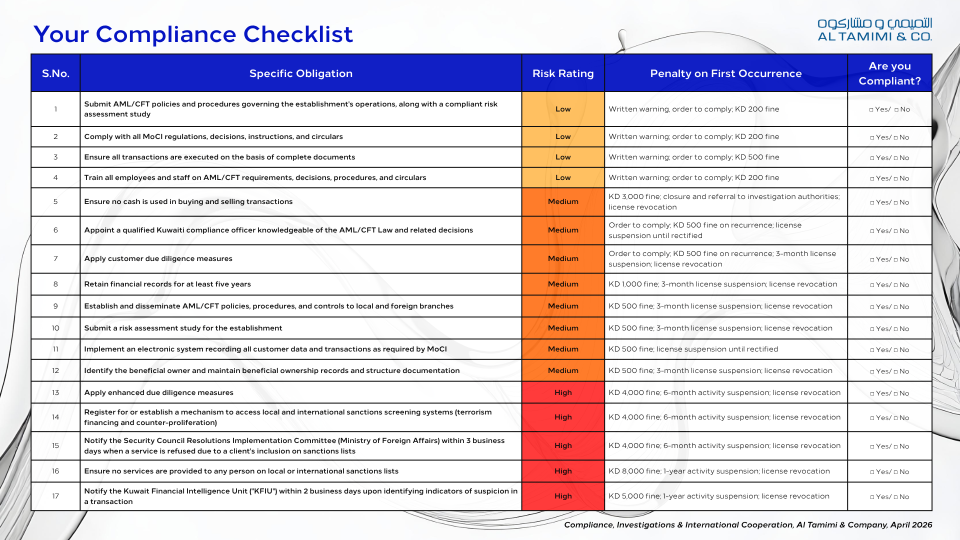

Compliance Checklist and Immediate Considerations

We have prepared the below compliance checklist for your reference to help you stay aligned with the enhanced regulatory requirements and to support your internal gap analysis. This checklist provides a structured basis for reassessing existing frameworks against the revised enforcement thresholds. Particular attention is likely to fall on medium and high-risk areas, where regulatory expectations are most concentrated and the consequences of non-compliance most acute.

Where This Leaves Businesses

Kuwait’s framework is evolving, and so is the scrutiny around it. The shift is not only regulatory. It is behavioural, operational, and increasingly external. The question is no longer whether expectations are changing. It is whether existing controls are keeping pace. In practical terms, weaknesses in controls are more likely to come to light, and when they do, the implications may extend beyond remediation alone. They may affect access to banking services, delay or disrupt transactions, and, in more serious cases, put licences and commercial relationships at risk. Businesses that treat this as a forward-looking adjustment, rather than a retrospective fix, will be better positioned to manage both regulatory exposure and the growing expectations of the market.

Key Contact

Ibtissem Lassoued, Partner, Head of Compliance, Investigations & International Cooperation, i.lassoued@tamimi.com